The COVID-19 pandemic has profoundly impacted the way we function as a global society. Particularly, our increased isolation and work-from-home environment has also significantly accelerated consumer online spending behaviours.

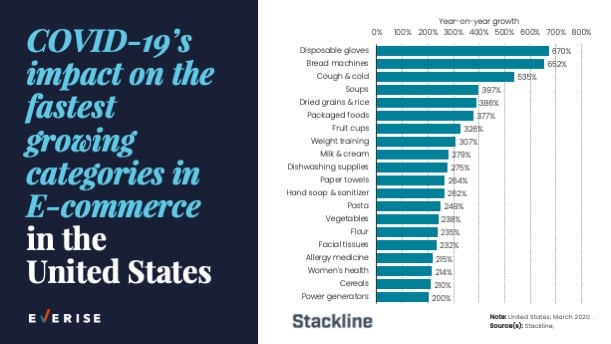

E-commerce has experienced a sharp increase in traffic with retail websites generating some 14.34 billion visits globally in March 2020. American consumers are buying everything from disposable gloves to bread machines to power generators.

Concerns over the use of cash aiding the spread of the virus encouraged more consumers to go digital. As of March 2020, a third of consumers in the United States expected they would increase spending on goods from online marketplaces. This new purchasing habit has equally impacted the Banking industry accelerating digital transformation initiatives.

Banks are already spending a lot of money on artificial intelligence (AI) and data analysis to pique the interest of the technology-savvy millennial class. With AI initiatives becoming more affordable to implement, banks now need to look at what added benefits they can provide and how they engage their customers.

Here are 3 areas that financial services should focus on:

1. Gamifying Financial Literacy

Game Thinking combines game design and design thinking to create an engaging experience that supports the learning process, whether in the form of a game or an interactive learning experience. Game-based learning is built around challenges to be mastered and applied, integrating learning content into the design process of developing the user experience.

Gamifying an experience aims to increase the time that people spend on educational content so that they will remember the material for longer. Apps like Duolingo show how gamification can help learners hold on to training for longer when learning a foreign language.

Banks have already employed this method to credit cards, awarding points when people purchase goods. Customers can claim those point for rewards in the form of travel perks, cash backs and a variety of different products. However, this is limited to credit cards. It's time banks take this idea and apply it to how people spend, save and invest their money.

For Banks, this method provides them greater reach as educational content integrates into the everyday functions that a banking app offers. By turning existing tools into a game, adding game elements like awarding points and badges when customers achieve something, banks can encourage users to use their partner merchants, while customers gain perks for using these strategic partnerships. By doing so, banks start to understand their customers better and can start recommending useful products to them.

2. Personalisation at Scale

Financial advice is something reserved for the top tier of banking consumers. These "preferred" customers have a high net value, and it is in the bank's interest to help them grow their wealth. But, where does this leave the average person?

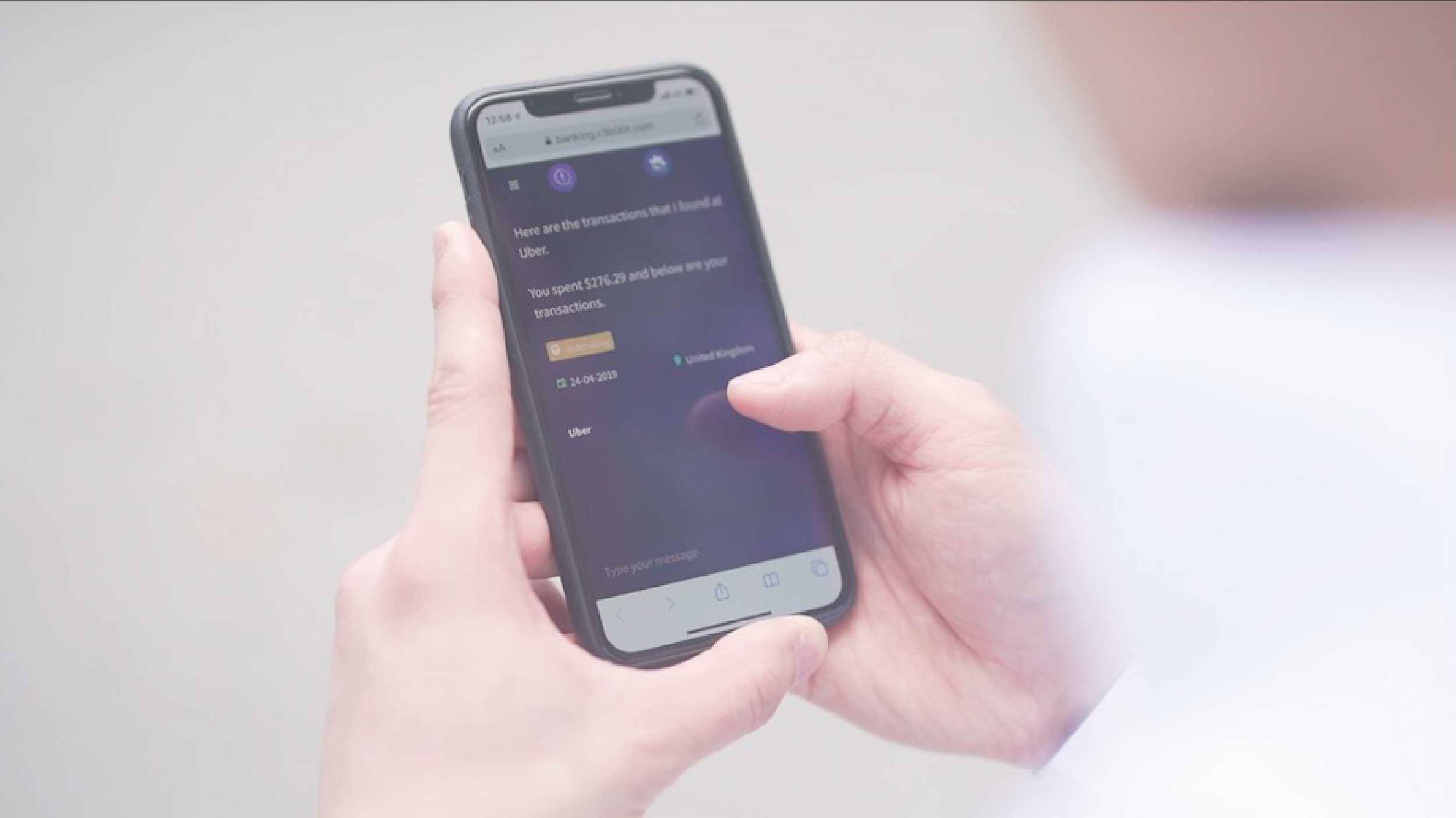

The everyday customer will benefit from intelligent analytics that could help them analyse and manage their money. The best way to deliver this tool is to use AI analytics. By reviewing individual users profiles, an AI programme can create a visual graph to help guide customers on how they spend their money.

Taking this one step further, by integrating conversational IVR or voice bots with account-level data, customers can have access to a financial advisor who understands their purchase patterns. This enables financial services to offer greater levels of service and personalisation at scale.

3. Predictive Recommendations

Curated content transformed the music industry catapulting companies like Spotify to the top of the download charts in app stores. They engage millions of listeners around the world, disrupting how people discover new songs and artist by recommending new content based on what users already like to listen too.

Intelligent curation of content is the ability to recommend the right content, or products at the right time. In the financial services industry, most products can be linked to significant milestones, the ability to predict their occurrence requires the ability to peer into purchasing behaviours.

This level of recommendation and insight into a user's financial needs is what AI has to offer a consumer. By using similar technology to understand how individuals spend their money, banks can help their customers achieve financial success using their products. Meanwhile, customers get more visibility on bank products, better service and less irrelevant advertising, thus improving their overall experience.

Investing in the Future of Banking Today

Providing banking advice is a relationship-building tool that relies on trust.

"I think what's really interesting, looking at the future of banking is how do we humanise banking in a way that a bank is your friend, but a friend with good advice and a bank that's going to help you essentially be better at earning money and spending money," says Vic Sithasanan, CGO, Everise DX.

By educating people on the best ways to maximise their banking experience with strategically placed game elements and predictive recommendations tailored to an individual's spending profile, customers can start to trust that banks are looking out for their best interest.

Using AI to provide this service at scale, exponentially increases a bank's ability to nurture positive relationships with its customers. As consumers reap the rewards of their new financial prowess, they are more likely to use the products that are recommended by the bank because they see the benefits it provides them and the lifestyle they want to lead.

Related Posts and Case Studies:

.png)